January 30, 2026

CAN AMTRAK BE PROFITABLE?

Last month we did a deep dive into the data behind freight and passenger rail traffic in the United States, noting that Amtrak has never had a single profitable year, and has lost $46 billion since its inception in 1971. For 2026, Amtrak requested a Congressional grant of $2.4 billion while promising to be operationally profitable by 2028. That is ambitious, to say the least, but according to international data, it might be downright impossible.

Of the top 130 rail systems in the world, only 31 are profitable. Japan, the first country to launch high-speed rail, operates 29 of them. The MTR in Hong Kong and the SMRT in Singapore are the only other rail systems in the world that are profitable. The London Underground is sometimes added to that list because it doesn't lose money, but that particular system just breaks even with fares, while the rest of London's mass transit loses money every year.

The average profitability of the top 130 rail systems in the world is a 30% loss. If the 31 profitable railways are removed, the average profitability of the remaining rail systems drops to a 60% loss. That puts Amtrak slightly better than the global average with an average 50% loss every year.

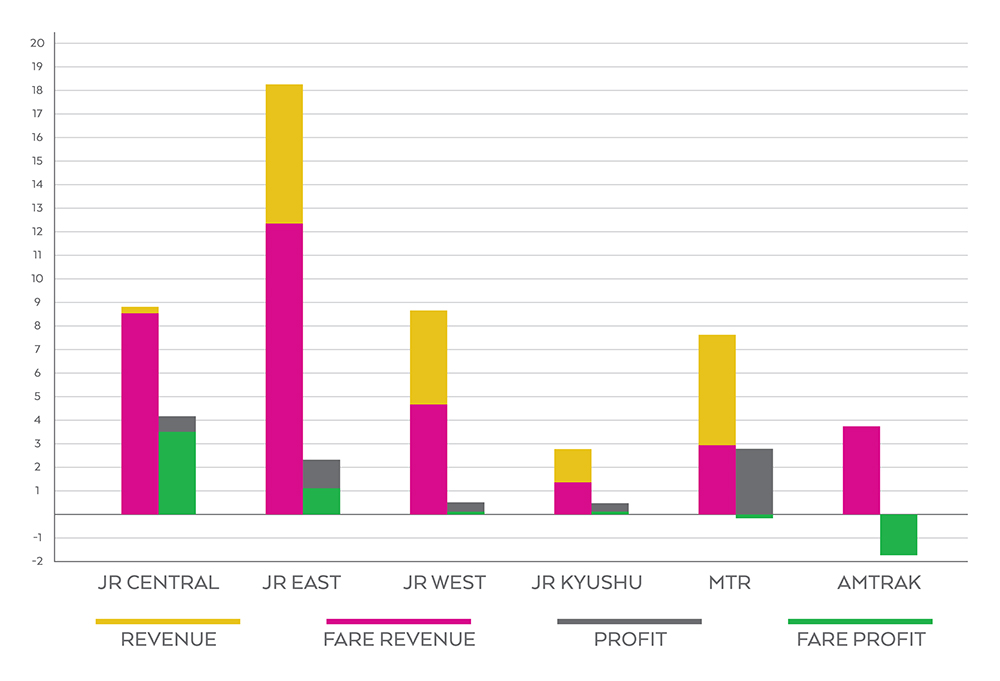

REVENUES AND PROFITS AS A PERCENTAGE OF FARES IN BILLIONS OF US DOLLARS

JR Central, the most profitable of Japan's 29 profitable railway companies, has become the envy and model for every other rail company in the world. Japan pioneered the concept of combining rail fares with other income streams like real estate and retail. But JR Central operates the most heavily traveled railway in the world, annually moving more passengers than American Airlines, the world's largest airline. The revenues it generates from rail fares account for over 85% of its annual profits.

But the same is not true for most of Japan's other rail companies. Of its other three large, profitable, passenger rail companies, JR Kyushu earns 57% of its profits from rail fares, JR East earns 46%, and JR West earns 29%.

Hong Kong's MRT modeled its rail transportation system after Japan, coining the term "rail plus property." Last year, it lost money in fares, but was still profitable due to its real estate revenues, demonstrating the power of diversification. Singapore's SMRT also operates other revenue-generating initiatives, but does not report unconsolidated performances for its business segments.

In light of these facts, what is Amtrak's plan to achieve profitability? In its appeal to Congress, Amtrak stated that it eliminated 450 workers and deferred other expenses in order to save about $100 million every year. Last year, the company lost $1.8 billion, so $100 million is not going to make a dent. Amtrak went on to detail a forecast for 2028, which centers on the Northeast Corridor. With a 25% increase in ticket revenues for just the northeast, and a continued federal grant of $2.2 billion ($500 million than it received last year) it believes it can achieve modest profitability. It is not expanding its revenue streams; it is not looking for non-transportation income; it is simply scaling its existing model, which has never come close to posting a profit.

But even if Amtrak were to somehow follow the Asian model of using real estate and retail to boost its rail profits, would that work? Recently, the Cato Institute reported on the economic history of Japan's high-speed rail development, revealing that when the country decided to privatize its state-run railroads into seven different companies in 1987 (much like Amtrak's creation in 1971), it ended up having to assume $400 billion worth of debt that those companies could never cover. In addition, the government continued to foot the bill for future high-speed rail constructions, hoping to recoup that investment by leasing the lines to the different rail companies. That investment has never been repaid. As a result, Japan accrued a huge amount of national debt, acquiring the highest debt-to-GDP ratio of any developed country in 2021 at 230%. Since then, the Japanese government has worked hard to rebuild its economy. Currently, Japan has the third highest national debt in the world, and it is still more than its GDP.

Hong Kong and Singapore also have some of the highest national debt as a percentage of their GDP, 456% and 383% respectively. There is no evidence that specific investments in high-speed rail are a major cause of this debt, but it is interesting that the two countries which followed Japan's example for rail profitability experienced the exact same economic pitfalls. The United States has the highest national debt in the world, representing 88% of its GDP. So it has no wiggle room for adding extra monstrous infrastructure projects without negatively affecting its own economy.

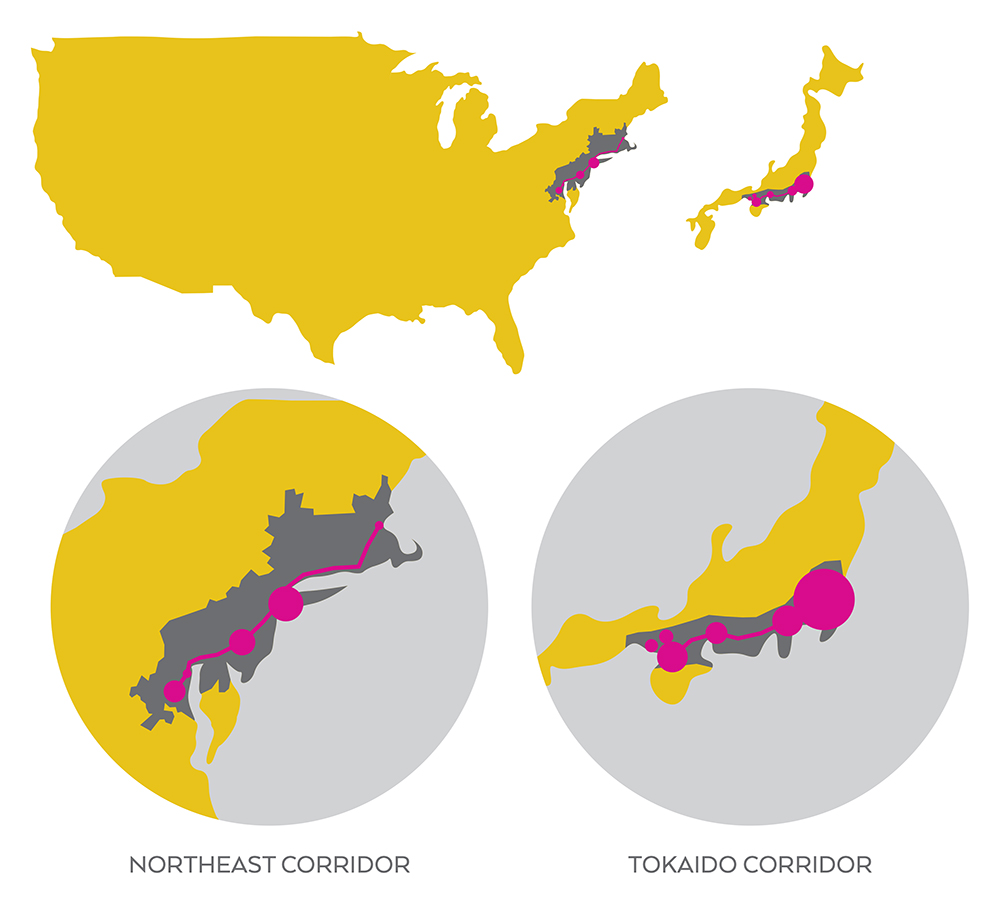

And adding to those considerations is the sheer size of Amtrak's territory. Currently, Amtrak is only profitable in the area known as the Northeast Corridor, a 320-mile-long section of railway that connects Boston to Washington, DC, and includes New York City, Philadelphia, and Baltimore. That section of the United States contains over 51 million people, representing 17% of the country's population. It is the oldest and most densely populated area of the United States. Comparisons are often made between the Northeast Corridor and Japan's Tokaido Corridor, a 350-mile-long section of railway that connects Tokyo to Osaka, and includes four other cities with populations over 1,000,000. It contains over 80 million people, and represents 70% of Japan's population. So while both corridors share very similar sizes and densities, their overall share of the national population is vastly different. It is highly unlikely that Amtrak could ever increase the profits of the Northeast Corridor to supplement the other 83% of the country's population.

NORTHEAST AND TOKAIDO CORRIDOR COMPARISONS

The largest problem facing a hypothetical profit increase like that is the current behavior and usage of passenger rail in the United States. Every year, of the 51 million people that live in the Northeast Corridor, Amtrak serves 14 million passengers. That is 27% of potential riders. In the Tokaido Corridor, where 80 million people live, Japanese trains serve 161 million passengers annually. That is 187% ridership. So due to Japan's size and culture, its densest rail corridor accounts for 53% more of the national population and 160% more ridership than the United States. Those numbers are not just overshadowing; they're downright overwhelming.

The United States is the third largest country in the world in both population and land area. Japan is 11 and 63 in those statistics. It is unrealistic to think the United States can model any kind of national transportation after a country with 219 million less people and three million less square miles of territory to connect. The only country in the world that can be used for comparison in both population and land area is China, and it does not operate a single passenger railway profitably. In fact, despite annual reports, it could be argued that no country does.

Maybe Amtrak can increase its revenues, and maybe it can decrease its losses. Maybe it can even get close to profitable. But the data seems to suggest that it is fighting a battle that has never been won. Perhaps its critics should take into account the unique landscape of the United States, and recognize that Amtrak operates the forty-second best financially performing passenger rail company in the world. It doesn't sound sexy, but it's better than bankrupting a country.

SOURCES

- "General and Legislative Annual Report" from Amtrak

- "Farebox Recovery Ratio" from Wikipedia

- "How We are Funded" from Transport for London

- "Lessons from Railway Privatization in Japan" from Tokyo Review

- "The Dark Side of the Bullet Trains" from the Cato Institute

- "Integrated Report 2025" from Central Japan Railway Company

- "Ten-year Statistics" from MTR

- "Countries with the Highest National Debt 2026" from World Population Review

- "NEC Facts and Figures" from Federal Railroad Administration

- "Interregional Travel: A New Perspective for Policy Making" from The National Academies

- "Country Comparisons - Area" from the CIA World Factbook

- "Country Comparisons - Population" from the CIA World Factbook

- Revenue data from various annual reports

LISTEN

SUBSCRIBE